Neuromarketing is the future

Fintech Marketing is extremely competitive, challenging, dynamic & expensive in nature. This leads to marketers constantly searching for innovative ways to capture the imagination of their prospective & existing customers.

The answer to this lies in the world of Neuromarketing & its correct understanding.

Neuromarketing is relatively a newer area of marketing that uses an individual’s reactive, emotional, and cognitive responses to understand, analyze, and predict consumer behavior.

Some examples of neuromarketing in Fintech & Banking include:

- Use of Color, symbols, images, calligraphy, and font to convey enhanced value, benefits, trust, security, and happiness

- Reduced Decision Paralysis through the optimal implementation of product & services

- Focus on Value vs Price, Benefits vs features for the products & services

- Create a sense of urgency through Loss aversion, FOMO & time-sensitive events & offers

- Extensive use of storytelling to create product demand by touching the latent needs & aspirations of potential & existing customers

- Use of anchoring strategies for offers & discounts as well as peer comparison

- Specific neuromarketing tools like eye gazing, physical validation through EEG, and facial recognition are employed to test & drive product uptake.

Let’s look at some of the neuromarketing tools employed in Fintech and banking in detail:

Color: Color is one of the most important response & emotion drivers for an individual. Different colors evoke different emotions, reactions, perceptions, and associations in an individual which can in turn invoke varied trust, engagement, and uptake of financial services & products. It should be kept in mind that colors have different symbolic attributes in different cultures.

- Blue: Blue is the most used color for banks and fintech as it is associated with higher confidence, security, and trust. It apart from being the universal color also conveys a sense of authority, professionalism, and reliability.

- Green: Green is the color of money, wealth & growth and it is natural for fintech & banks to use this in abundance. Additionally, green is also identified as safe, secure, and trustworthy in many cultures and evokes a huge positive response from customers. It is also a visually pleasing color that evokes nature, abundance, and calmness. Green can help fintech products and services convey a sense of value, benefit, and opportunity. Most fintech uses green in some form to connect with the customers. Example: Chime, Robinhood, Acorn, Lili, zest

- Purple: Purple denotes luxury & opulence and while less common, it’s used by fintech & banks to differentiate products on luxury, innovation, and royalty parameters. It is also a distinctive color that can help fintech products and services stand out from the crowd. Purple can help fintech products and services convey a sense of exclusivity, creativity, and sophistication.

- Other colors like Yellow, Red, White, and Black are also used by banks & fintech based on the individual brand ethos, design, identity, target segments, and product features.

Decision Paralysis: Being spoilt for choice is not always the best option. When customers are bombarded with multiple products & features, they get overwhelmed psychologically and at times fail to reach a decision, impacting their behavior, attitude, and satisfaction towards a product or company. For Fintechs & banks, this is of high importance as providing multiple options may lead to a delayed or canceled transactions.

Some examples of decision paralysis in Fintech are:

- Similar product options: For Fintech marketplaces, this is a very common but serious issue as hot leads generally get delayed as customers get confused with similarities and value differentiation between various products while trying to obtain the most optimal bargain. For example, if a bank offers dozens of credit cards with different features, fees, and rewards, the customers may feel overwhelmed and give up on choosing one.

- Too much detail: Providing unnecessary and added information that is at times contradictory and irrelevant to consumers may overwhelm them in their understanding of product features & benefits. For example: Providing too many numbers, charts, and graphs that are inconsistent or confusing may result in frustration, and disinterest in customers.

- Tedious & Complex process: Asking too many questions, or a tedious process with too many steps may annoy customers and affect their decision to close the transactions. For example, if a bank asks for too much personal or financial information that is not essential or secure, the customers may feel uncomfortable and quit the process.

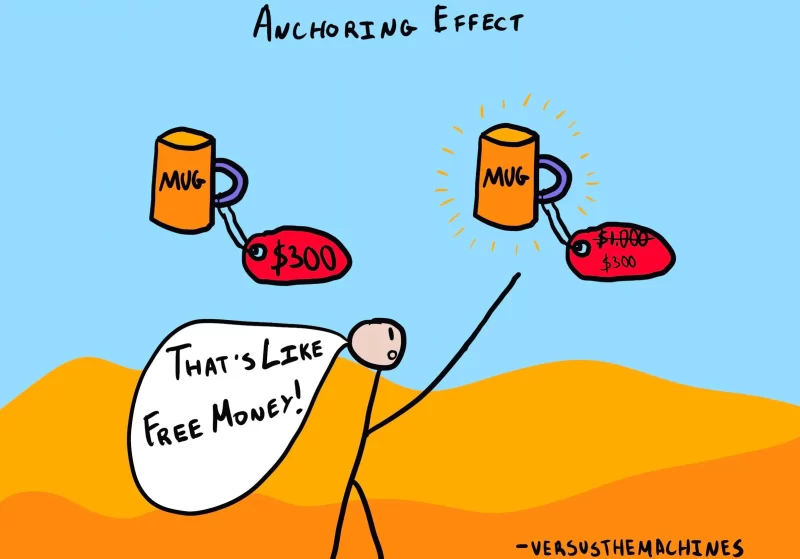

Anchoring: Anchoring is a cognitive bias and a great neuromarketing tool used by fintech & banks to show value offered to their customer base. By providing an initial reference point like price or number, and using this for making subsequent judgement.

Few examples of anchoring in Fintech & Banking:

- Discounts & offers: Using competition pricing or previous pricing as an anchor and providing a discount or offer over that pricing to boost sales

- Interest rates: When we compare different loan or deposit options, we may anchor on the interest rate and ignore other factors, such as fees, penalties, or terms. For example, if we see a loan with a low interest rate, we may think it is a good deal, even if it has high fees or a short repayment period. Similarly, if we see a deposit with a high interest rate, we may think it is a good investment, even if it has low liquidity or high risk.

- Savings goals: When we set our savings goals, we may anchor on arbitrary numbers or round figures, such as $10,000 or $100,000. These numbers may not reflect our actual needs or preferences, but they may influence how much we save and how satisfied we feel with our progress. For example, if we set a goal of saving $10,000 for a vacation, we may stop saving once we reach that amount, even if we can afford to save more or need more money for the trip.

- Negotiations: When we negotiate with banks or other financial institutions, we may anchor on the first offer or counteroffer that is presented to us. This can affect how we perceive the fairness and attractiveness of the deal and how willing we are to compromise or walk away. For example, if a bank offers us a low interest rate on a loan, we may think it is a generous offer and accept it without further negotiation. Conversely, if a bank offers us a high interest rate on a loan, we may think it is an unreasonable offer and reject it without considering other aspects of the deal.

Loss Aversion: Another psychological neuromarketing tool that relies on the customer’s tendency for loss avoidance more than acquiring gains. This is used in conjecture with FOMO (Fear Of Missing Out) to persuade customers to make early purchase decisions.

Some examples of this in banking & fintech include:

- “Don’t let your money sit idle. Earn up to 5% interest with our savings account and avoid losing hundreds of dollars every year.”

- “Protect your family from unexpected expenses. Get our life insurance today and avoid leaving them in debt or hardship.”

- “Take advantage of our limited-time offer. Apply for our credit card now and avoid missing out on rewards, cashback, and discounts.”

It should be noted that this strategy needs to be used sparsely and cautiously as it may result in customer disinterest as well.

There are various other neuromarketing tools and strategies employed by Fintech & bank including facial expression recognition, eye tracker, heat map, packaging, and usage of Neurotest to recalibration of advertisements & features.

Key insights from:

- Fintech Marketing in 2024: Strategy, Trends, and Examples

- 10 Ways Fintechs Are Using Experience Design To Outcompete Banking

- Getting your fintech brand right: stand out with color

- How to choose a color for your fintech brand

- The Psychology of Color in Financial App Design

- Loss Aversion Marketing: When Loss Aversion Works … – ActiveCampaign

- Loss aversion: The important role of this effect in marketing – IONOS

- The power of loss aversion in marketing – Hype insight

- Loss Aversion Marketing Tactics and Strategies That (Still) Work – Braze