BNPL (Buy Now Pay Later) is the buzz word in the payment industry with lot of interest from online and offline retailers. A recent study by Mckinsey has pegged BNPL growth at 100% from $92B to $182B between 2019 to 2023. Almost all retail giants including Amazon & Walmart have either their native products or tied up with partners for BNPL services. A recent study by Mastercard has shown that a BNPL activated E-commerce site has 35% less probability of cart abandonment & 45% increase in average sales from existing relationships. Globally, BNPL players like Klarna, Affirm, Square (Who also acquired Afterpay recently) has seen huge growth in recent years. Affirm tieup with both Amazon & Walmart for BNPL has raised lot of eyebrows in both e-commerce & payment industry. In India, BNPL has gained traction in both online & POS model with companies like Capital Float, Simpl, Lazypay, Zest Money leading the race in pure BNPL players in addition to likes of OLA postpaid, Postpaid by Paytm, Flipkart pay later & Amazon pay later.

There has been a lot of discussion and noise of BNPL taking over the Credit card & PL with few pandits even predicting a full takeover with credit card becoming obsolete in next 3-4 years. Should Credit Card or Personal Loan companies be terrified?

Let’s start with understanding the specific advantages BNPL has over other payment methods.

- BNPL’s most important advantage is it’s ability to provide the cashless transaction facility to a larger underbanked society with limited or no exposure to credit. These people will generally be ineligible to apply for the card or loan from regular channels. Extension of credit / EMI at fixed fee has led to creation of a new segment of customers. The real competition for these customers are from companies like Bajaj Finserv for their CD loan products and unstructured NBFC small ticket personal loans for Educational / Travel purposes.

- Another advantage of BNPL is ease of documentation with almost null income document requirement. The limit is basically decided on the bureau history and kyc of the customer.

- Additional advantages are Fixed cost and low interest vis-a-vis credit cards EMIs or revolves.

- So Basically it provides the advantages of a personal loan with credit card like features

So again the same question: Aren’t Personal loans or credit card in danger of being obsolete?

Well, the answer is a confident NO. BNPL, Credit Card & Personal loan may look like targeting the same market & customer segment but in reality, all three have their own customers and market with only a small part intertwining between each other.

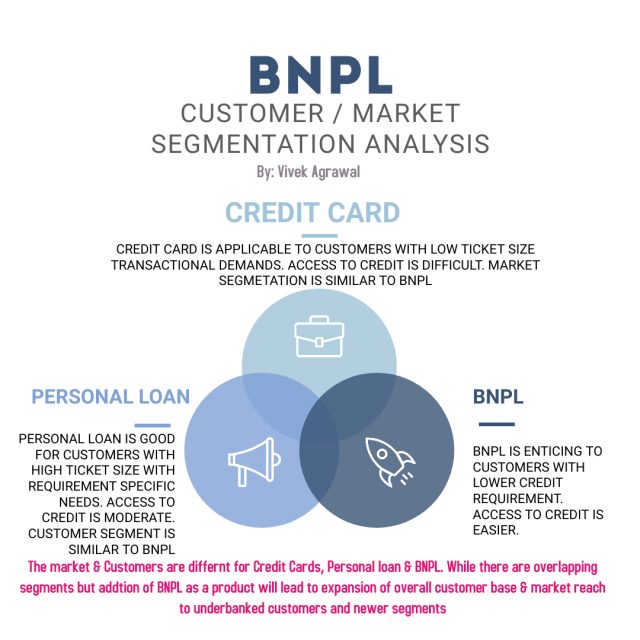

Let’s look at the customer & market segmentation of each product

Credit Card: Credit Card caters to a small / large ticket purchases with easy conversion to EMI. Most of the customers are transacting and EMI decisions are taken later except for POS EMI conversion. Also, the tertiary benefits by using the credit cards in terms of rewards, acceptance in much higher. The target customer segment is Credit Savvy users with occasional EMI needs. The target market segment is generally low to medium ticket size. The recurring documentation needs are not there.

Personal Loans: Personal loans caters to high value cash requirement for purchase / non-purchase needs. This is a need based product with acceptance to higher interest for personal use. Persona loans are also taken to meet emergency requirements. The documentation needs are specific to each loan and customers needing a personal loan are generally Credit hungry customers. The target market segment is generally high ticket size.

BNPL: BNPL caters to a third segment with customer segmentation similar to Personal loan and market segmentation similar to credit card. This category of customers were generally either ignored or were forced to go through one of the two previously mentioned products (with extremely high failure rates). The rise of BNPL has led to creation of a new category of users with defined customer and market segmentation. The Credit requirement is low to medium ticket size backed by a product purchase and behaviourally higher credit hunger due to lack to credit exposure.

The rise of BNPL is a good thing for the payment industry as it will lead to the credit exposure to a broader customer base who were largely skipped by regular CC & PL companies. This will have a waterfall effect on the product with increased movement to other segments like Credit card & PL by these customers based on their credit history. BNPL as a product has already forced the segments to start innovating and we have card companies coming up with fixed fee based instalments; companies like Visa & Mastercard planning their BNPL foray and lot of innovations planned in personal loan segment. While the BNPL is a good thing overall in terms of expansion of universe, the credit card & PL companies have to be on their toes to run with the same pace of innovation to ensure sustenance in long term.